BrianAJackson/iStock by way of Getty Photographs

Funding Thesis

The ink was barely dry on my final publish for Searching for Alpha about Viatris Inc. (NASDAQ:VTRS) – during which I instructed the corporate makes for a wonderful “purchase” alternative, given its exceptionally low worth to gross sales ratio of 0.75x, free money movement per share of ~$2.1, which interprets to a price-to-FCF ratio of ~5x, and dividend of $0.11 per share paid for the ultimate 3 quarters of 2021 – when Viatris elected to promote its biosimilars division to India-based Biocon in a $3.3bn deal. This precipitated its share worth to fall by 35%, from $15 all the way down to $9.80.

In my final publish, I had highlighted Biosimilars as one of many key strengths of Viatris’ enterprise mannequin, commenting that:

A biosimilar is similar to a generic, however its organic profile shouldn’t be similar to the drug it’s making an attempt to mimic – as long as the efficacy and security match the drug, nevertheless, the biosimilar can get round among the restrictions that apply to generic medication.

Viatris believes there may be ~$161bn of present revenues up for grabs, if biosimilars might be dropped at market that precisely match the efficiency of the medication whose mechanism of motion (“MoA”) they’re designed to imitate.

A few of the targets already lined up by Viatris are compelling. In July, the FDA accepted Viatris’ Semglee – an insulin glargine biosimilar of Sanofi’s (SNY) Lantus, a drug that after earned peak gross sales of $7bn each year, albeit lower than $1bn in 2021.

Hulio – a biosimilar of Humira, AbbVie’s (ABBV) >$20bn each year promoting anti-inflammatory remedy – has been launched in Canada, while biosimilars in growth embody variations of Regeneron’s (REGN) $8bn each year promoting Eylea, Botox and a spread of most cancers medication.

In equity, Viatris shouldn’t be chopping its ties utterly with its biosimilars division. Biocon has been a long-term associate of Mylan, the Netherlands-based specialist generic drug developer whose merger with Pfizer’s spin off of its Upjohn legacy manufacturers division created Viatris in November 2020. As a part of the sale, Viatris will take a 12.9% fairness stake in Biocon by way of $1bn of convertible most well-liked shares.

Viatris may also have a seat on Biocon’s board, and help in a deliberate 2023 IPO. Nonetheless, it’s clear that Viatris’ administration divested the Biosimilars division on the first out there alternative. This offers buyers some much-needed perception into what kind of firm Viatris is, and as importantly, what kind of firm it is not.

Brief Time period Income and Asset Gross sales, Not Biosimilar R&D

These hoping that Viatris would prioritize forward-thinking biosimilar drug growth, and make investments closely in R&D to attempt to change the prescription drug panorama, will clearly be dissatisfied.

Anyone who’s shopping for Viatris inventory for extra pragmatic causes – to learn from excessive margin gross sales of legacy drug manufacturers earlier than they’re changed by newer manufacturers, or swallowed up by generics, for a beneficiant dividend, and at an exceptionally low cost share worth – will in all probability have taken the information – and the share worth dip – much better.

Biosimilars weren’t a core a part of Viatris’ enterprise. Complicated generics and biosimilars accounted for under $1.34bn of $17.8bn of revenues in 2021, or 7.5%. Viatris will maintain onto its advanced generics after the deal, which is scheduled to finish within the 2nd half of this yr.

Administration argues that finishing the deal for $3.3bn complete consideration – which is 16.5x projected 2022 EBITDA, and three.8x projected revenues, makes good enterprise sense. It argues it is a optimistic motion in gentle of the corporate’s 3 level “speedy execution” plan to reshape the enterprise, comparable to level 1 – “unlock worth and simplify out enterprise” – the others being to “speed up monetary flexibility” and “construct a sturdy, greater margin portfolio.”

It’s a pragmatists’ want listing, and a method that can virtually definitely contain additional asset gross sales – as much as $9bn by 2023, together with the Biocon deal, Viatris administration hopes. The corporate already has earmarked one other $4-$6bn of merchandise it will be comfortable to half with. Administration additionally speaks optimistically about creating world, vertically built-in companies by means of these gross sales, starting with biosimilars.

Debt Too Urgent A Concern Not To Make Additional Gross sales

On condition that Viatris has set itself the objective of paying down $6.5bn of debt by 2023, having paid off $2.1bn in 2021, maybe the Biocon deal was the one method of conserving tempo with its deleveraging objectives. Given its Q421 earnings presentation, which suggests the corporate has $23bn of debt, or 3.5x EBITDA, it’s simpler to see why administration shouldn’t be playing on biosimilars changing into the following huge factor, however conducting an asset sale as an alternative.

That’s in step with the present biotech bear market situations, and it additionally makes it clear what sort of firm Viatris is. As talked about above, it’s a firm centered on shrinking in measurement and changing into extra worthwhile. It isn’t centered on speculative R&D and difficult for share in new markets.

Does that make Viatris an excellent or a nasty funding? As talked about, information of the Biocon deal despatched Viatris’ share worth down by ~35%. Nonetheless, the inventory has gained barely since, rising to a worth of $10.7 on the time of writing, with a market cap valuation of $12.94bn. I believe the share worth will proceed to rise.

There’s a worry round Viatris that it’s valued so low relative to gross sales and free money movement as a result of it has been set as much as wind down or get rid of Pfizer’s failing UpJohn legacy property, while making an attempt to revive the fortunes of generic drug producer Mylan. In some ways that is true, and the Biocon deal underlines it.

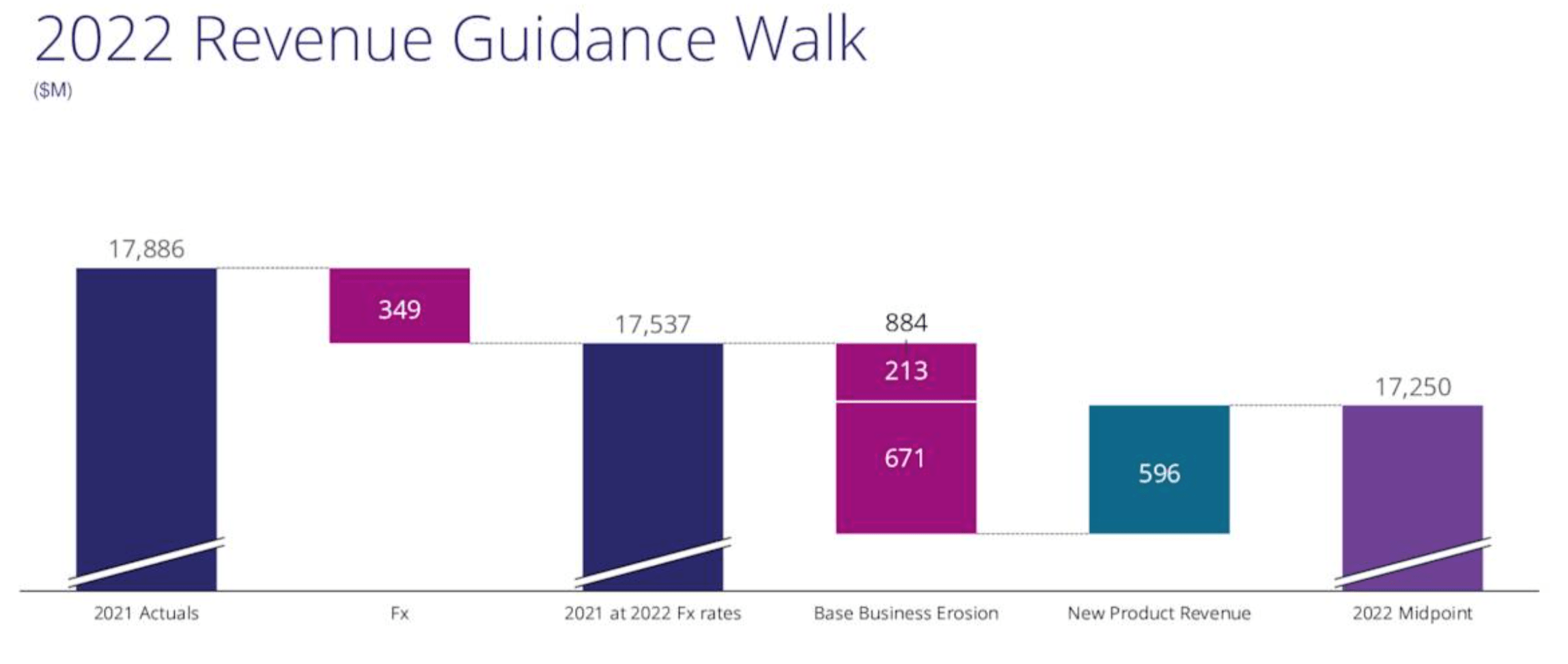

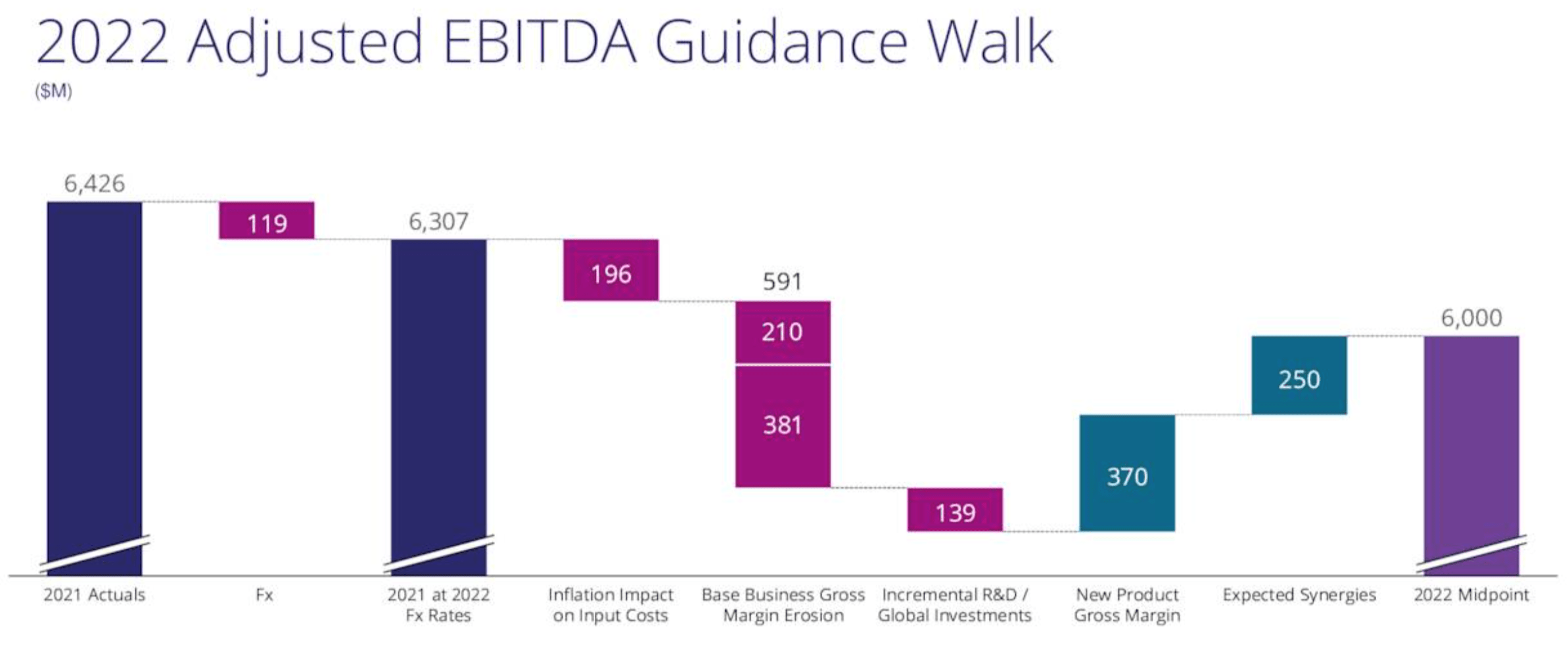

Though this enterprise mannequin could not supply a lot of a pipeline, or a lot long-term sustainability, it is troublesome to argue that it’s not engaging within the brief time period. There’s a large debt pile to cope with, however Viatris generated EBITDA >$6bn final yr, on revenues of $17.9bn, and expects to do related once more in 2022, as proven beneath.

Viatris FY22 Income Steering Stroll. (earnings presentation)

Viatris FY22 adjusted EBITDA steerage stroll. (earnings presentation)

Paying off $2bn of debt utilizing EBITDA / deal value synergies, and, to illustrate, $2bn utilizing asset gross sales every year for the following 3 years would halve Viatris debt place. It could additionally convey internet debt to EBITDA down to shut to 1.5x, all while the corporate pays a dividend that provides a present yield of 4.5%. This isn’t a nasty proposition for a potential shareholder.

It is Not All Doom and Gloom on The R&D Entrance – Though All the things Is Doubtless On Sale

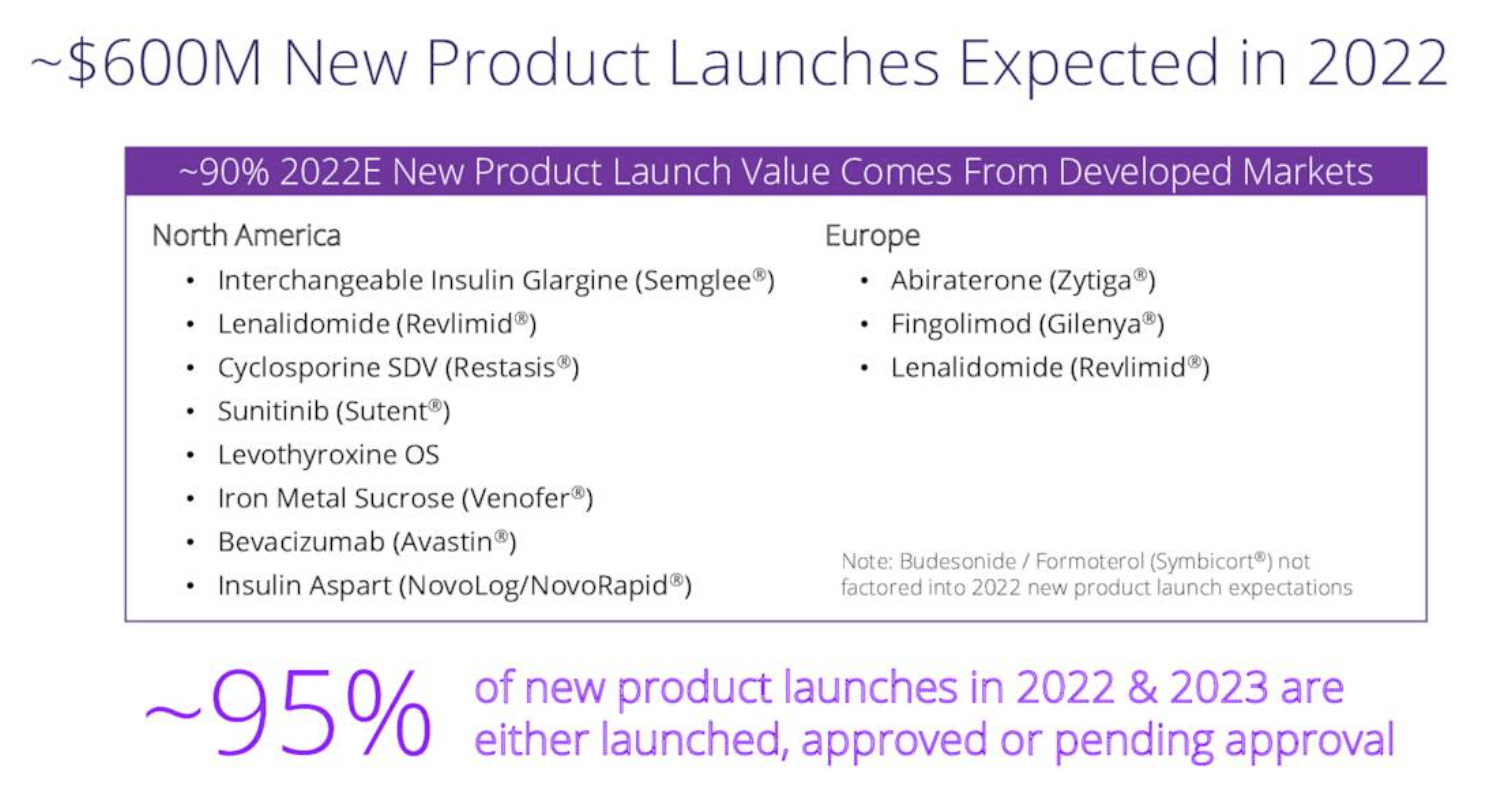

Though I’ve been vital of Viatris’ capacity / want to develop new income streams, there will probably be ~$600m anticipated contribution from new merchandise subsequent yr, from a comparatively wholesome Generics pipeline, as proven beneath.

New Product Launches slated for 2022. (earnings presentation)

There may be extra to return in addition to, with 5 extra merchandise anticipated to launch in 2023, together with a generic model of blood thinners Xarelto and Eliquis. The latter is likely one of the high 5 greatest promoting medication on the earth, 6 in 2024, most from the advanced generics pipeline, and eight in 2025 and 2026.

There is no telling if Viatris could promote its advanced generics enterprise in 2022 or 2023, nevertheless. However, once more, even when administration does try this, advanced generics doesn’t presently pull in a lot income – between them, core generics – $5.6bn. Established manufacturers – $10.84bn – introduced within the overwhelming majority of Viatris’ $17.8bn of revenues final yr.

Manufacturers Are Viatris’ Bread & Butter & Gross sales Are Holding Up

Viatris makes 61% of its gross sales in developed markets, and 60% of all of its gross sales are from its established manufacturers. So, there may be nothing revolutionary concerning the firm’s enterprise mannequin.

Though, in time, some established manufacturers could lose market share in, e.g., the US and Europe, as new medicines arrive with a superior efficacy / security profile, their gross sales should still improve in rising markets that can’t afford to pay high greenback for his or her medicines.

Having lengthy since gone off patent, the likes of Lipitor, Lyrica, Norvasc and Viagra are nonetheless producing >$500m revenues each year. That is $1.7bn each year within the case of ldl cholesterol reducing Lipitor, so buyers shouldn’t be overly involved about sudden declines in Viatris’ high line revenues – at the least for the remainder of this decade.

Of extra concern is the sheer quantity of medicines Viatris have to be coping with. Ten of its most profitable manufacturers account for under ~$6bn of revenues, the earnings presentation suggests, which leaves $10bn extra income generated from property seemingly incomes ~$100m or much less.

That have to be a problem operationally, though Viatris does profit from a worldwide infrastructure constructed by Pfizer and Mylan. This may assist it to scrap successfully for market share for brand spanking new launches, and fiercely defend current share around the globe, while additionally ready for markets akin to China to open up.

Conclusion – Viatris Will Hold Rewarding the Pragmatist, Disappointing the Biotech Fanatic

Once I final lined Viatris I used to be evaluating the corporate’s inventory with one other spin-off firm, Organon & Co. (OGN). This was fashioned after Merck divested its biosimilars, Ladies’s Well being, and Established Manufacturers divisions into a brand new entity.

In an earlier word on Organon, I wrote:

Contemplating its present valuation relative to its gross sales, you would virtually forgive Organon’s administration group for taking a hands-off method, and specializing in conserving gross sales of its 49 totally different Established Manufacturers worthwhile as revenues slowly shrink within the face of generic competitors, returning a pleasant revenue to shareholders by sustaining product sales margins, presently 65%.

To summarize many of the above dialogue, I really feel equally about Viatris – that you would hardly blame administration for promoting off what it might of its lesser income producing property, while guaranteeing gross sales of established manufacturers are optimized. Within the course of, this generates revenues and income that make a mockery of its $12.5bn valuation – lower than 0.8x projected FY22 gross sales.

After the sale of its most dynamic, promising division to Biocon to lift funds to pay again debt, I feel buyers now have a a lot clearer image of the route Viatris is headed in. It’s seemingly going to get smaller in measurement, operationally streamlined, and fewer indebted. It isn’t going to speculate closely in new market alternatives, new medication, or intensive R&D.

I can perceive buyers’ issues on that entrance – how are you going to purchase an organization that’s not going to develop, the place is the worth? However the corollary to that argument is the outdated Benjamin Graham investing mantra:

Within the brief run, the market is a voting machine however in the long term, it’s a weighing balance.

What I imply by that is that, when Viatris first started buying and selling in November 2020, and thru its first investor day, it was judged by buyers when it comes to what they anticipated the corporate may be, or what they hoped it may very well be. Viatris could properly show to be a disappointment on that entrance.

However because the voting machine offers strategy to the weighing balance, it is vitally exhausting to look previous $17bn of projected revenues in FY22, and a market cap valuation of $12.5bn. That form of worth is just not on supply elsewhere within the biotech or pharmaceutical sectors, or certainly in every other sectors.

That is why, in my opinion, buyers in Viatris can proceed to gather the dividend, and extra seemingly than not, profit from regular progress within the share worth, punctuated by the occasional sharp fall at any time when a brand new asset sale is organized. The worth proposition is sufficiently good at the moment to outweigh issues about how a lot Viatris will shrink within the subsequent 5-10 years.

It could take rather a lot for Viatris to carry out badly sufficient as an organization to justify its present low market cap valuation. Though I feel buyers may have to time their exits proper in the long run, I plan to proceed to carry my Viatris inventory for a 3-5 yr interval. I can’t panic when the corporate sells of chunks of the enterprise, and look elsewhere to seek out progressive biotech firms.

Viatris is not a type of – its shares are merely superb worth at present worth, I imagine.